“Investment Committee ABC” By Alexander Degwitz For The NMS Management Investment Bulletin for the Endowment & Foundation Community January 2018

Migrating from a patriarchal governing system — common in early generation family businesses, where a single per- son is responsible for most decisions — to an institutional one where a group has to effectively reach agreements and execute decisions can be quite a feat. In the short term, it is “easier” and there is tremendous propensity to leave things in the hands of the willing leader when results are often adequate if not great and beneficiaries can keep a free pass to remain in their comfort zone, receiving distributions while having limited or no responsibility. Sounds ok, yet status quo in this condition means future generations remain disempowered, dependent and ill-prepared to handle their wealth; “Some 70% of family-owned businesses fail or are sold before the second generation gets a chance to take over. Just 10% remain active, privately held companies for the third generation to lead.”(George Stalk, Jr. and Henry Foley, Harvard Business Review FROM THE JANUARY-FEBRUARY 2012 ISSUE, “Succession Planning, Avoid the Traps That Can Destroy Family Businesses” P.1). In the long term, the patriarch will not be around and survival of the family business (FB) will depend on developing functional and well-institutionalized groups that can transcend, where the right to participate is not entitled but earned and where there is a strong desire amongst beneficiaries to stay together. Stable governance groups can reduce the peaks and valleys of the spectrum of the individual human cycle, permitting more predictable and consistent conditions to prevail, which is the desired environment for businesses to succeed.

To achieve long term growth, a system of governance should evolve from a “Control Model” characterized as a governance system where “control rights are not fully separated from ownership, ownership tends to be concentrated and sees conflict of interest as endemic and seeks to institutionalize them or provide sanctions for them rather than eliminate them”, to something more attuned to a “Market Model-board structures and practices that ensure that the board is a distinct entity, capable of objectivity and able to act separately from management”(Joseph Astrachan, Andrew Keyt, Suzanne Lane and Kritsi McMillan. “Loyola Guidelines for Family Business Boards of Directors” P.3). This migration of governance model is often a consequence of the family’s transition from a sibling partnership where governance is highly reliant on leadership of strong family individuals to a cousin consortium in which proliferation of partners demands stronger institutions to maintain a balance amongst partners whilst increasing the relative weight of professional managers vis-à-vis ownership.

In my understanding, it is generally healthy to shield businesses from the often-irrational and personality-infested issues that families face. I can refer to a common case of what I consider a distortion in a management system whereby the same people who are responsible for ongoing concerns are responsible for managing liquidity. This mixture of roles and responsibilities without clearly defined parameters and procedures for capital disposition is likely to have negative consequences for both liquidity and business management: 1) Decision criteria for portfolio management may be unduly influenced by the money demand of the FB and 2) The effect of the proverb “necessity is the mother of invention” is jeopardized.

Dependence on cash to operate results in an inverse correlation between cash availability and capacity to produce creative business solutions. To cure this condition a clear separation of governance for ongoing concerns from liquidity management is recommendable. In essence, the relationship between the two should be one whereby the Board Of Directors (BOD) of businesses solicits funds to the Family Office (FO) by demonstrating that it can produce better returns than those produced by investment portfolios and risk tolerance parameters allow further concentration of investment in the FB.

In my understanding, it is generally healthy to shield businesses from the often- irrational and personality- infested issues that families face.

An FO can be organized as the executive arm of the family, to manage family affairs, investments, tax planning, property management, concierge services, etc. Its governance criteria can be similar to that of a normal Board of Directors (BOD), as it is responsible for over- sight of what is often the fuel that sparks growth in the FB: liquidity. According to a friend and Wal-Mart USA ex-CEO Bill Simmons, the role of a BOD is simply to “provide direction”. The asset management governance system of the FO can benefit from the same basic purpose and beliefs that guide a BOD. A simple example of some of our family guiding principles can illustrate how these can be equally relevant to both BOD and FO.

Guiding Principles that we aspire to live by:

“Our enterprises and their assets have the fundamental purpose of creating the conditions for their stakeholders to develop their full potential.”

“The will of the group will always prevail over the will of any of its members.”

“We are responsible custodians to the wealth of our descendants.”

The most significant role of an FO is to organize an asset management capacity typically under a governance structure commonly called Investment Committee (IC). This body can be composed of members of the family and/or its businesses (internal members) and external ones that should be experienced money managers. Even though familiarity with financial markets should prevail, branch representation will often be the main driver in the selection process. Overlap between BOD and IC membership should be limited to avoid conflict of interest. The Family Council (FC) should appoint members for renewable terms to reduce trauma associated to rotation of family members. As is the case with the bylaws of a corporation that defines the rules of engagement of a BOD, it is important to create an operating agreement for any IC.

Often, the first job is to simplify and consolidate an unnecessarily large amount of legacy accounts into two or three fundamental portfolios based not on the origin of the funds but on the objectives each serves, for example:

◆ Capital Preservation Fund, intended to be a “rainy day fund” with a relatively conservative profile and longer-term horizon, intended to guarantee payment of dividend to beneficiaries and cover cash deficits or investments as solicited by FC.

◆ Operational fund, intended to have a more liquid and less volatile profile, destined to provide support to businesses.

◆ Foundational and/or Educational Fund, intend- ed to guarantee financing for philanthropic initiatives or education of members of the family and its enterprise leaders.

The IC has a long-term strategic goal and should be cautious not to take a chronically opportunistic approach to how it makes decisions. The IC should procure a disciplined approach to managing asset allocation based on portfolio goals and avoid regularly altering strategic course with the evolution of the markets. In our fam- ily we implemented an active asset management system whereby our in-house investment team bought and sold positions in single name bonds and equities from many geographies following strategies recommended by banks and experienced family members. I have seen intense work placed in keeping up with benchmarks, subjecting portfolios to significant volatility and unnecessary stress to the shareholders resulting from markets swings.

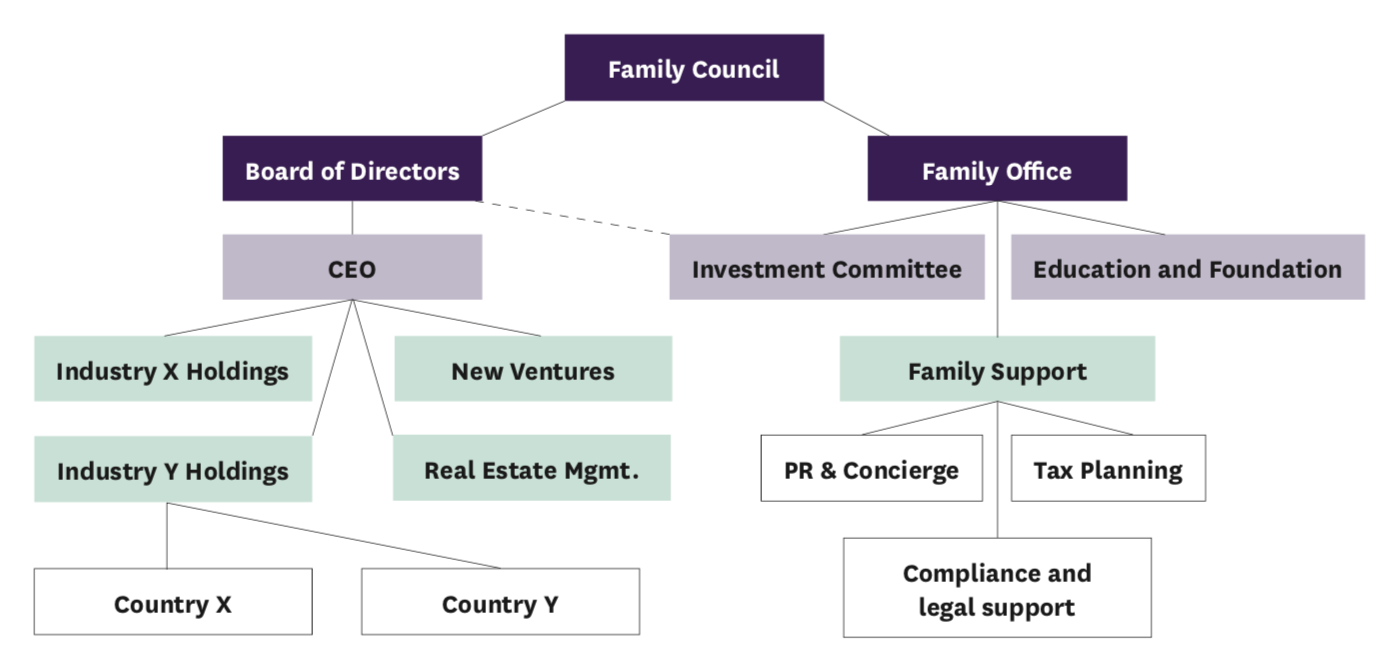

(Figure 1)

In our case, following recommendation of the BOD, we engaged an outsourced asset manager to handle our liquid portfolios and eliminated our in-house team.

The main reasons were:

◆ Size Our wealth did not merit full time staff for asset management.

◆ Experience Proven professionals are likely to out- perform in-house staff. Professional institutions should have a fully dedicated team with institutional knowledge, expertise, resources and market connectivity; hire the best money managers in each asset class.

◆ Objectivity Separate teams for analysis and IPS development from trading execution is recommend- able; making portfolio decisions may be cumber- some when executors are employees.

◆ Confidentiality risk It is difficult to keep a tight lid on sensitive information when personnel are permanently exposed to colleagues in other areas of the family companies or in a country where such information can be used against owners’ interests.

The IC has to understand family needs clearly and be ac- countable for implementing decisions, define overall strategy and risk tolerance for portfolio managers. This can be done by way of an Investment Policy Statement (IPS), which should be proposed by the IC and approved by the FC. This tool provides explicit parameters to define types of assets and the allocation to each. It should also con- template the entire asset base of the family, as one should limit additional exposure to risks one is already exposed to. As per discussions with a friend, Gregory Curtis — Founder and Chairman of Greycourt & Co. — an IPS is a living document, which in plain language should guide investment policy both over the long and short-term. It should include:

1) Investment Objectives the purpose for the funds, general risk tolerance, and important factors for the family such as geographies, leverage, volatility, loss of corpus etc.

2) Performance Objectives can be described in terms of absolute return (i.e., 5%) and/or relative return as compared to a composite benchmark that has a similar volatility or asset class composition to the allocation in the portfolio.

3) Distribution/Spending Policy what and when are the family’s draws required.

4) Definition of Investment Advisors as well as selection/retention criteria.

5) Performance Measurement and Review defines reporting content and periods as well as bench- marks associated with each asset class or manager.

6) Asset Allocation Targets defines how return goals will be reached.

7) Investment Manager Evaluation Criteria

investment style, risk profile and organizational stability are as important as performance in choos- ing money managers.

8) Modification policy defines the procedure to re- vise and change the IPS as well as mandating periodic review. The Operating Manual and the IPS Statements should have balanced rigidity to provide fundamental structure and dynamic parameters to allow enough discretion to respond opportunely to the market changes.

The result should be an empowered IC with an effective decision-making body and a system capable of evolving well with financial markets.

The example in Figure 1 contains a possible structure to reflect the interdependence amongst the three primary governing entities. The FO is a very broad concept implemented differently by each family, yet most have asset management as their core purpose, which is why a solid Investment Committee institution is central to the FB organization. There is no single solution for all, but often one’s experience can help others find their own way. I have seen highly successful FBs that have dysfunctional FOs and vice versa. Do not let this discourage you, take the opportunity to use the structure of the stronger one to rethink and rebuild the weaker one. To transcend over time and serve as good stewards to the wealth of our descendants, having well defined roles and well regulated FB and FO are aspirations all families should strive for.